Are you acting your age when it comes to your money?

We need to recognize that when it comes to our money, we must act our age. What I mean by that is that the level of risk we are taking on in our portfolio needs to be consistent with how much time we have in front of us to leave our money alone to recover from a major market correction before we will need to access it for retirement income. This is particularly true after we retire. Academic research is continuing to demonstrate that for those taking income in retirement primarily from equities, the performance of the portfolio in the early years of retirement will often tell the tale as to whether the retirement account will live as long as the retiree. If the early years are fundamentally good ones in the markets, then despite taking income for retirement, the account has the chance to grow and be better prepared to deal with the inevitable rough years in the market that will one day come. If on the other hand, the early years of retirement are negative years in the market, a combination of withdrawals for income and losses in the market can create a hole that can be very hard to climb out of. Van Harlow, director of research at the Putnam Institute, says succinctly: "One of the biggest risks to a successful retirement is the exposure of savings to one or more adverse negative investment returns in the early stages of retirement."

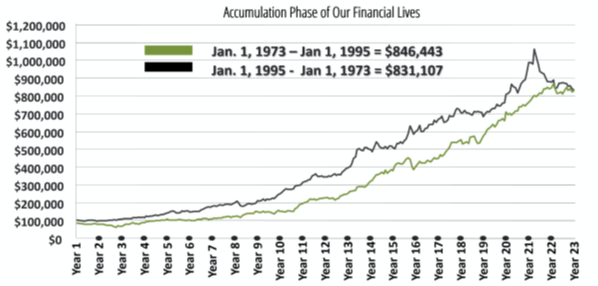

The charts that follow offer a very hypothetical example of how "sequence of return risk" can work against the retiree. The first example is of two people (we'll call them Jack and Jill) who were both in the accumulation phase of their lives. Jack (represented by the green line) invested $100,000 in a 50% stock/50% bond portfolio over a 23-year period from 1973 until 1995. He enjoyed a 10.1% average rate of return, and his money would have grown to $846,443. The early years for Jack were not good ones in the market, and the latter years were very good, but it really didn't matter because he wasn't taking withdrawals. In the case of Jill (represented by the black line), all we have done is reversed the sequence of returns, so that 1995 was her first year, 1994 her second, on down to her last year of 1973. She also enjoyed a 10.1% rate of return, and her money grew to $831,107…almost the same amount as Jack. Unlike Jack, in her case the good years came early, and the bad years came late, but once again it didn't matter because both she and Jack were in the accumulation phase of their lives and were not taking any withdrawals.

The accumulation phase of our lives is very different than when we enter the distribution phase of our lives at retirement. As we have seen, when we are younger the sequence of our returns doesn't matter a whole lot. Additionally, when we are younger, we have a much longer time frame to recover from market losses. A market correction when we are 35 years old does not impact our future retirement in the same way it might impact a 60-year-old person who is nearing retirement age. In the accumulation phase of our lives, "ROI" is all about "return on investment." We are primarily pursuing growth because we are years away from needing our investments for income and we have a lot of time to recover from market corrections. When we are older and in or near retirement, those same three letters "ROI" come to be more about "reliability of income," because we are now at a place where our investments need to help fund our retirement lifestyle. And when income begins to be withdrawn during the distribution phase of our lives, the sequence of the returns we receive can matter a great deal.

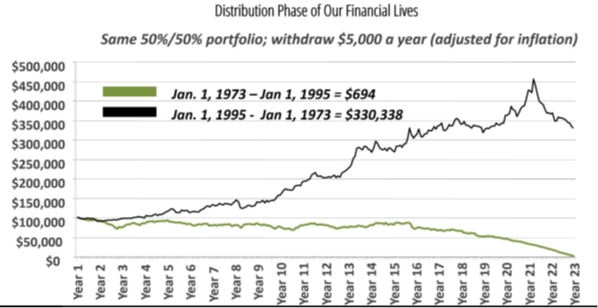

In our second hypothetical example, we are keeping all of the variables the same except for one. Jack and Jill both still start out with $100,000. Both still have portfolios that are 50% stock and 50% bonds. Both still invest for 23 years, with Jack being invested from 1973 to 1995, and Jill simply having the years reversed so that she is invested from 1995 to 1973. The only difference is we now begin to have them withdraw 5% ($5,000) each year for retirement income. Remember, in the first example, Jack has some lousy years at the beginning but great years at the end, while Jill has great years at the beginning and lousy years at the end - but it didn't matter. Why? Because they were not taking withdrawals. But now, by adding income withdrawals into the equation, look at the difference in outcomes:

In this case, Jack ends up being essentially out of money at the end of 23 years, while Jill enjoys income for the entire 23-year period and still sees her initial $100,000 amount more than triple in value. And the remarkable thing about this huge disparity in outcomes is that they both enjoyed the same rate of return of 10.1%! Jack had the bad luck of starting to take out income right as the market was going down, and was essentially having to sell investments while they were down in value every time he cashed a monthly retirement income check. In those early years, Jack was "digging a hole with two shovels," by both withdrawing money and losing money on his investments. This put his portfolio on a downward trajectory that he was never able to reverse. Jill, on the other hand, was lucky enough to enjoy solid gains in her portfolio in the early years, so that her account grew in spite of her withdrawals, creating a buffer against the inevitable difficult market years that eventually came.

The value of being age appropriate when it comes to risk and retirement can be summed up by the simple observation that when we retire, we are not looking through the rearview mirror at the certain past, but rather must gaze through the windshield into an uncertain future. We don't know if we are retiring at a lucky time or an unlucky time, and so we must allocate our money accordingly.

One tool that can be very effective in establishing contractual confidence when it comes to our retirement income is a fixed indexed annuity. An annuity is essentially life insurance in reverse. We buy life insurance in case we die too soon and want to make sure we provide for our loved ones. We buy an annuity in case we live too long to make sure we can provide for ourselves. Like all financial products, annuities have both pros and cons associated with them and they are certainly not for everyone, but in the right scenarios they can be a very effective tool in mitigating against the risk of running out of income in retirement. The value of an annuity in an overall retirement plan is the ability to create some income predictability for your retirement future. Jeffrey Brown, a professor at University of Illinois at Urbana-Champaign and a co-author of the research paper "Framing Lifetime Income" says: "Guaranteed lifetime income, such as in the form of annuities, is incredibly valuable for retirees. It is the single best way on a risk-adjusted basis to maximize one's ability to spend in retirement without concerns about running out of resources. Every other strategy either exposes the individual to more risk or reduces one's ability to consume."

It is important to establish what the goal for retirement is. If we define success as "whoever dies with the most toys is the winner," then we may take on additional risk to achieve that goal. But if our goal is to wisely manage our financial resources in order to live with confidence the only retirement that we are ever going to have, then we only want to take risks that are necessary to the achievement of that goal.

You would probably never set out on a journey without first having a pretty good idea of where it is you wanted to go. It is not much different when it comes to planning for your retirement. On a very personal level we need to think through what it is that we want to do and accomplish in retirement. Lee Eisenberg in his bestselling book, "The Number," wonders aloud about why people do not plan for retirement. He asks, "Could it be that in the end the reason we don't plan is because we don't have anything meaningful to plan for?" What is it we want to do when we step away from our work? Do we want to travel more, spend more time with our children and grandchildren, be more engaged in our church or with charities? Perhaps you made your living as an engineer but what you always really loved was art history…do you go back to school to pursue that love? The late Steven Covey, in his book "The Seven Habits of Highly Effective People," talked about the need for us to "begin with the end in mind." Rather than stumbling through your retirement years, ask yourself, "At the end of my life, when I look back at my retirement years, what do I want to be able to say about how I spent them?" Apart from having a defined goal of what we want to do in retirement, the years can just slip away as we spend our time engaging in things that do not engage our hearts. To quote the poet Goethe, "Things which matter most must never be at the mercy of things which matter least." WeTirement is here to connect you with someone who may be able to help you address your retirement income needs, concerns, and questions.

©2022 Tarkenton Financial LLC. Fixed indexed annuities are products of the insurance industry. Annuities are not FDIC insured. Guarantees in insurance products are based solely on the financial strength and claims-paying ability of the issuing company. This article is not intended to provide specific guidance or recommendations for your individual financial situation. Speak to a qualified financial professional for guidance on your individual situation.