We are all familiar with the concept of ‘sequence of returns’ risk: the idea that the sequence in which the investor experiences returns in the early years of retirement is crucial to whether the investor will have enough money to last the rest of his or her life. We know that positive returns during the early years of retirement will greatly improve the investor’s chances of not running out of money. We know that negative returns early in retirement drastically reduce the likelihood of an investor having money at the end of their life. But why is that, exactly? Well, it’s because it is difficult to make up for the losses incurred while the investor is also withdrawing money for income. But how difficult? To know exactly how devastating sequence of returns risk can be, we must first understand what it takes to make an investor whole after a loss. Let’s look at the math.

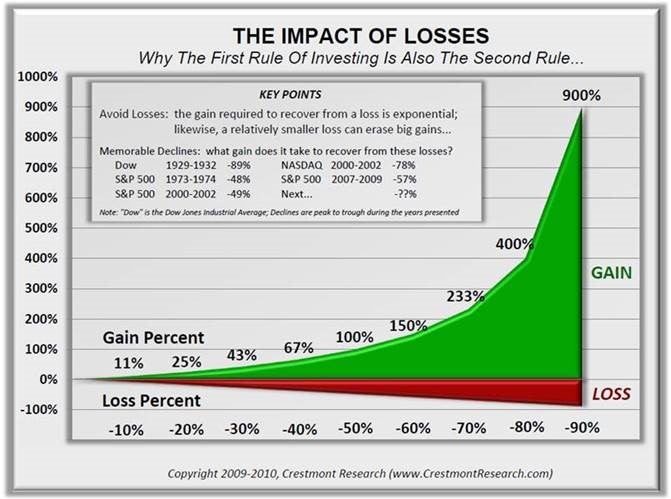

The first thing to know is that the percentage gain needed to make an investor whole after a loss increases exponentially as the amount of the loss increases. Below is an equation you can use to calculate the percentage return needed to make an investor whole after a loss:

y = x/(1-x)

y = percent gain needed to make investor whole

x = percent decline

So, let’s look at a couple of examples. First, let’s look at the Great Recession (’08 financial crisis). The market fell about 57% from 2007–2009, so the percentage return needed to make an investor whole after suffering through that time period was 133%. The equation looks like this:

1.33 = .57/ (1-.57)

After the crash of 2008, it took the S&P 500 six years to get that 133% and get back to where it started pre-crash.

Second, let’s look at the Tech Bubble crash. The NASDAQ fell 78% from 2000–2002. That’s 355% to get back to where the investors started! You can see how quickly this can get out of hand. It took the NASDAQ 15 years to gain the 355% that it needed to break even with a 78% loss. Whoa. Let’s think about that a different way. We plan for retirees to live about a 30-year retirement. That means the NASDAQ took HALF of the average American’s retirement to recover. And that’s with no money coming out for inflation-adjusted income.

The third scenario we will look at is the Great Depression. The Dow had an 89% loss from 1929–1932. What does it take to recover from an 89% loss? 809%! That is incredible. So even though the Great Depression valley was only 11% lower than that of the Tech Bubble crash, the percentage needed to break even in the Great Depression is 454% more than that of the percentage needed to break even after the Tech Bubble burst.

I don’t want to beat a dead horse; however, below is a graph illustrating the point I just made with the historical examples.

How do we avoid these crashes and “corrections” harming our retirement? Well, very few Americans can afford to fund their retirement without the stock market and the compound interest it can give us. However, as each of us approaches retirement, we need to avoid the big losses that can, and most likely will, happen. Carving a portion of one’s assets into a fixed indexed annuity can provide a guaranteed income stream or a decent growth opportunity, both without downside risk of the stock market. It is important to contact your marketer to find out which product is right for your client’s financial situation. Read on for a sales idea on how to use this concept with a client.

Sales Idea:

Take a look at your client’s portfolio. Look at what it did from December 1st, 2018, through December 31st, 2018. Then use the equation in the above blog post to calculate how much the client needs to earn to get back to where they were at the beginning of December 2018. Once you have that number, ask the client if they are confident the market will do that or better in 2019. If they answer “no,” you can ask them if they would like to place a floor on how much they could lose. If they answer “yes,” ask them how confident they are. Then ask them, if they were able to place a floor on how much they could lose, would they take it? A lot of times, when you have these conversations, your clients will convince themselves that they need some downside protection in their portfolio. But you have to educate them first on what the actual impact of a down market is on their portfolio.

Thank you for reading,

Dustin Casebolt

Director of Advisor Development