To Diversify or Not to Diversify

Can we agree that investors should diversify their portfolios across asset classes? Can we also agree that the reason investors diversify across asset classes is to manage risk and portfolio volatility? So, what if you are investing in a fixed indexed annuity, where you can’t lose money to market losses? Do you still need to diversify? Does the reason you need to diversify change? Let’s think about it this way: when you diversify across asset classes in the market you are doing so to mitigate risk because different industries and asset classes can react differently than others to the same events. Which would mean that some asset classes will make more money than others in the same market conditions. Thus, increasing your chances of making a gain somewhere in your portfolio. So, what does this mean for fixed indexed annuities?

Well, Great American has long been the carrier that has indexing crediting methods that follow different indexes than just the S&P 500 or the, harder to find, more complex, proprietary indexes. For example, the iShares U.S> Real Estate ETF or the iShares MSCI EAFE ETF; but now Great American has released a product that has one of the shortest durations on a fixed indexed annuity with some reasonably high caps. The surrender schedule is only 3 years. That’s right 3 years and your money is free and clear. You have the opportunity to select between a declared rate (2.35% for high band), iShares U.S. Real Estate annual ptp with cap (5.75% for high band), S&P 500 annual ptp with cap (4.6% for high band), or iShares MSCI EAFE ETF annual ptp with a cap (5.25% for high band). These rates are as of 5/13/19.

A lot of market analysts are predicting that the last 10 years of the market growth is not likely to happen over the next 10 years. Instead of averaging 6.793% like the S&P 500 has over the last 10 years; we should expect more like 3-4% annualized average over the next 10 years. So, maybe it is time to look at other ways to help our clients safely accumulate returns? Let’s look at these other ETF’s that Great American offers crediting strategies on. The MSCI EAFE has averaged 4.38% since 2002. The iShares U.S. Real Estate ETF averaged 6.44% over that same timeframe. And to compare apples to apples, the S&P 500 averaged 6.65% since 2002. Now, these are huge homerun returns but let’s look at what would happen if we had allocated to the other crediting strategies.

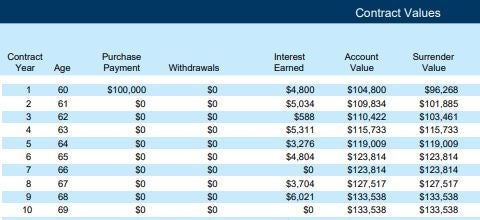

You can see from the hypothetical illustration above, there were only two years over the last 10 that your clients would receive a zero on their statement. With this hypothetical illustration, I used $100,000 premium, with 50% into the S&P 500, 35% into the iShares Real Estate, and 15% into the iShares MSCI EAFE. The important thing to remember about this product is that it is a 3-year surrender schedule. So, in this case, you put in $100,000 and at the end of the surrender schedule you can pull out $115,733. That’s over a 15% return in three years. Not too shabby.

If you believe the market will continue to climb for the foreseeable future, by all means, use a product that is more lucrative. If you don’t think the S&P 500 will continue to soar, then maybe you should consider some alternatives. All while continuing to keep you clients principal protected. Give your Tarkenton Financial marketer a call to learn more about this new product from Great American.

Thanks for reading,

Dustin Casebolt

Director of Advisor Development