The Retirement Hierarchy of Needs, Part 2

This blog post is the second of a series on what we at Tarkenton Financial call the “Retirement Hierarchy of Needs.” The Retirement Hierarchy of Needs is a philosophy of how to build a comprehensive financial plan for a client. The idea is to make sure to cover all of the needs, wants, and risks that may arise in a client’s retirement. Let’s look at the hierarchy.

With each tier of the hierarchy comes different types of expenses or goals for the money. You work with the client to determine how much money you need to allocate to each tier. In each post of the series, we will look at a different tier. We will discuss what expenses or risks are included in that tier and look at different ways to solve for those expenses.

If you read the previous post, you are familiar with the different tiers. In today’s post we will cover the “Want to Haves.” This tier is composed of the more flexible expenses we have in life and, specifically, retirement. These expenses, again, need to be defined by the client. These expenses will vary greatly depending on the client – and clients have a tendency to under-estimate these expenses. A good practice is to go through line items of their monthly expenses to make sure you are getting an accurate picture of everything they are spending. Here is another obvious tip, if they aren’t saving money, they are spending money. So, if there is money not accounted for in their savings or “Need to Haves” then, you can count it as “Want to Haves” expenses. There will be some non-recurring expenses like vacations or trips. I know for some people these are a must (my fiancée says we have to go on at least one international trip a year), so it is important to understand where these expenses fall on their priority list. Again, once you have an annual “Want to Have” number, you can back into the different financial product/strategy that will best meet the client’s needs.

Let’s look at another case study. We will use the same assumptions of income, age, and investment timeframe (55yo, Male, needing $20,000/yr in “Want to Haves”, retiring at 65). We will again be comparing four different financial products/strategies to solve for the “Want to Haves” number. These strategies include:

- Equities portfolio and bond ladder

- REIT

- Variable Universal Life Policy

- Indexed Universal Life policy

We will again be comparing different areas or factors for each strategy, including:

- Investment Needed

- Balance after 20 years

- Total Income after 20 years

- Total Fees after 20 years

- Total Taxes Paid on the income after 20 years

Since these are not guaranteed expenses, we are not going to be looking at “worst case scenario” assumptions. For each strategy there will be slightly different assumptions, that will be described in each section. For growth on the Equities, VUL, and IUL, we will assume 6.9% growth. This is the growth rate that a lot of IUL illustrations show as the most recent 10-year period average rate.

Equities Portfolio

So, first things first, the equities portfolio is assuming an average annual growth rate of 6.9% and a withdrawal rate of 2%. I am also assuming a long-term capital gains rate of 15% and an AUM fee of 1%. I didn’t use a zero-growth scenario for this exercise, as I did for the ‘Need to Haves’ post, because the idea is these expenses are flexible. If we have a down market, we don’t have to take the money out to use on these expenses. With the equities portfolio, the math is fairly simple. You need $513,124 at age 55 to grow 6.9% a year for 10 years to get your $20,000/year in income. Your client also ends up paying more to you (their advisor) and the IRS than they receive in income over the same period of time. That doesn’t seem quite right. Don’t get me wrong, I am not opposed to equities portfolios. They are just not the most efficient way to generate income. Let’s look at two different scenarios that will demonstrate how much more powerful an equities portfolio can be without an income drag on the performance.

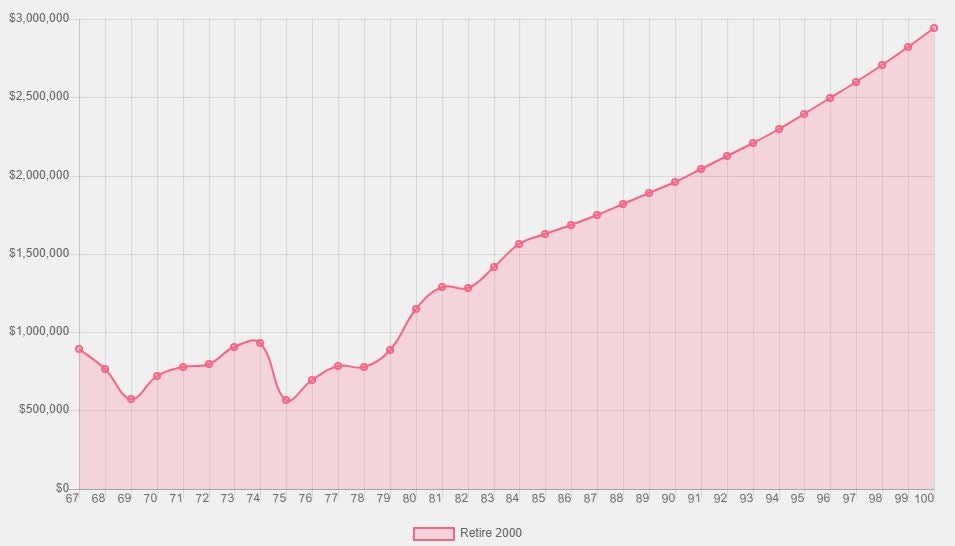

You can see in the above chart that if we are pulling $20,000/yr out of a $1,000,000 portfolio it does fine. In this chart, I used historical S&P 500 rates from 2000 to 2018 and then assumed 5% a year growth. At age 100, the client has $2,943,843. Now take a look if we had carved out the insurance premium each year starting 10 years prior.

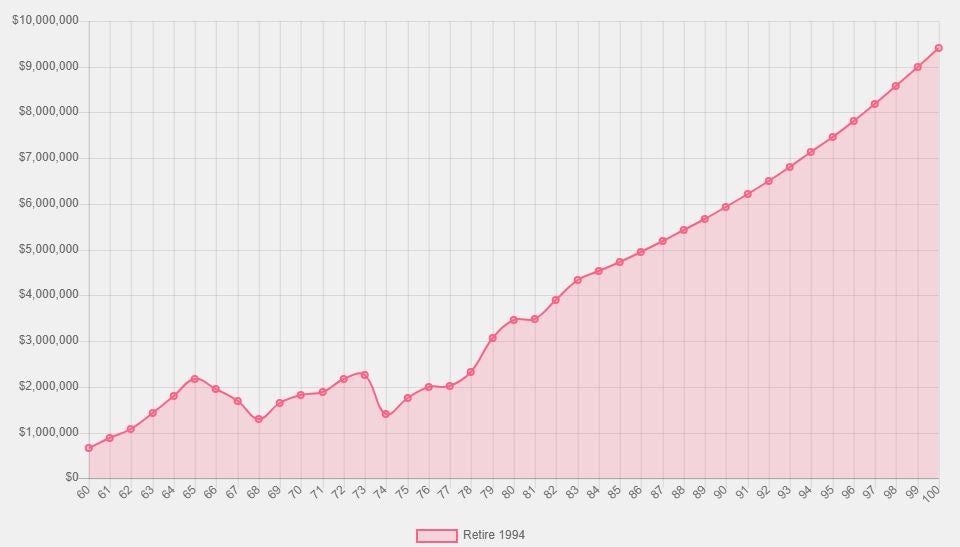

Now, in the above chart you see a scenario where we have been funding the IUL by pulling $18,000/year out of the equities portfolio from 55-65 years old. You can see, again using historical S&P 500 return until 2018 and then using 5%, the client would be left with $9,420,001 in their equities portfolio at age 100. Those numbers should speak for themselves.

REITs

A client once told me, “I like REITs, they are like an inexpensive annuity.” There is a lot wrong with that statement, but I can understand the idea. REITs have an underlying asset and pay a dividend. A lot of times fueled by lessees’ payments. These can be a steady source for income. There is one problem: the word “can.” The real estate market in America has rebounded nicely since 2008, which helps a lot of people forget about what happened to a lot of REITs in and around that time. To keep the dividend where the REIT company originally set it, they lower the share price (I am referring to close-ended REITs in this example). So, as the underlying value of the REIT decreases, so will the dollar amount of the dividend payment. All that being said, let’s look at the numbers from the comparison chart from earlier in this post. I took an average dividend payment from some major REIT companies and it came to 5.25%. So, if we back in to the principal required for $20,000 a year in income; that puts us at $380,952. We will also assume that the principal will not grow or lose value. So, besides making the argument that it takes less money in an IUL to generate the same amount of income from a REIT; the other factor to consider is taxes. The tax number for the REIT strategy is a number based on the dividends from the REIT being fully taxable capital gains. This number does not exist in a void, however. The $20,000 a year in income received from the REIT would be taxed at capital gains rate (I assumed 15%) and that income is also factored into your client’s adjusted gross income (AGI). AGI will be factored in when determining how much of your client’s Social Security benefit is taxable. This could greatly affect how much money your client takes home. As Benjamin Franklin famously said, “Only two things in life are certain: death and taxes.” The only control we have over taxes is when we pay them. In my opinion, it is generally better to pay taxes now rather than later. As explained in my previous blog post, “Let’s Talk About Tax, Baby.”

VUL

The argument for IUL’s over VUL’s is similar to that of an FIA over a VA. It’s all about the fees and efficiency of your client’s money. If you look at the table at the start of this blog post, you can see that the VUL policy requires a higher total target premium, over the first ten years of each policy, than that of the IUL. In fact, $63,990 more. Sure, your client is left with more in the cash value at 20 years, but your client has also paid $35,810.62 more in cost of insurance and policy fees. If you do the math on the illustration I used for this case study, specifically on the money in versus the money paid out and in the cash value at year 20; the VUL has a 36% return over 20 years and the IUL has over a 51% return over the same 20 years. Again, this is taking income received and cash value left in the policy. Another way to look at it would be that at year 18 of the IUL policy you are “in the money.” Not until year 23 of the VUL policy would you be “in the money.” Here is the kicker: this scenario is if the VUL policy doesn’t have a negative return in the 20 years of this case study. A negative year, or two, could destroy the way the VUL performs.

Conclusion

Just like the first tier of the Retirement Hierarchy of Needs, the ‘Want to Haves’ tier may not have one correct answer, because any of the above could work, but it does have one strategy/product that is the most efficient use of your client’s money. Call Tarkenton Financial today to give us a chance to help you with your clients’ retirements discretionary spending needs. You can reach us at 800-659-4942.

Thanks for reading,

Dustin Casebolt

Director of Advisor Development

Tarkenton Financial