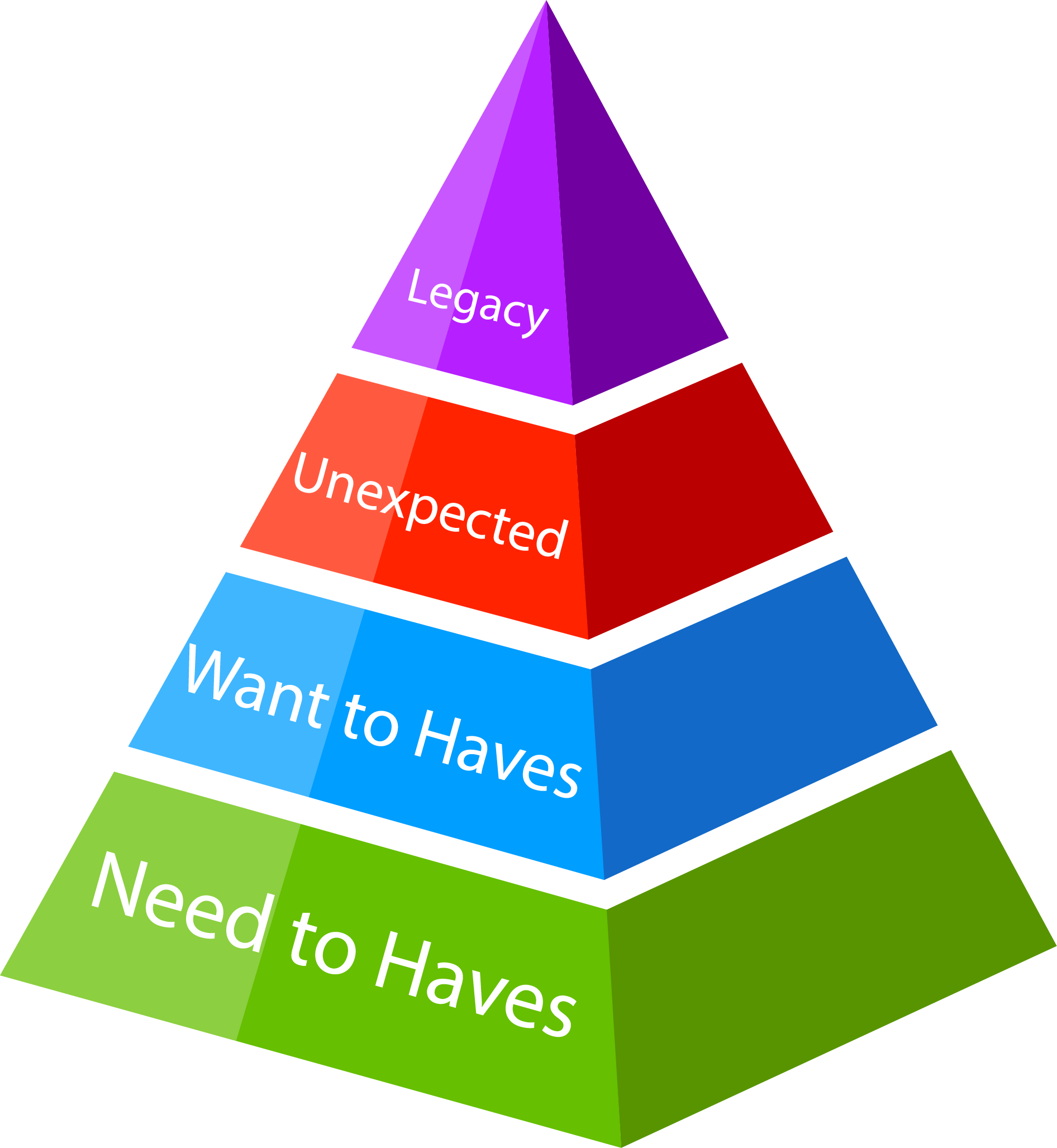

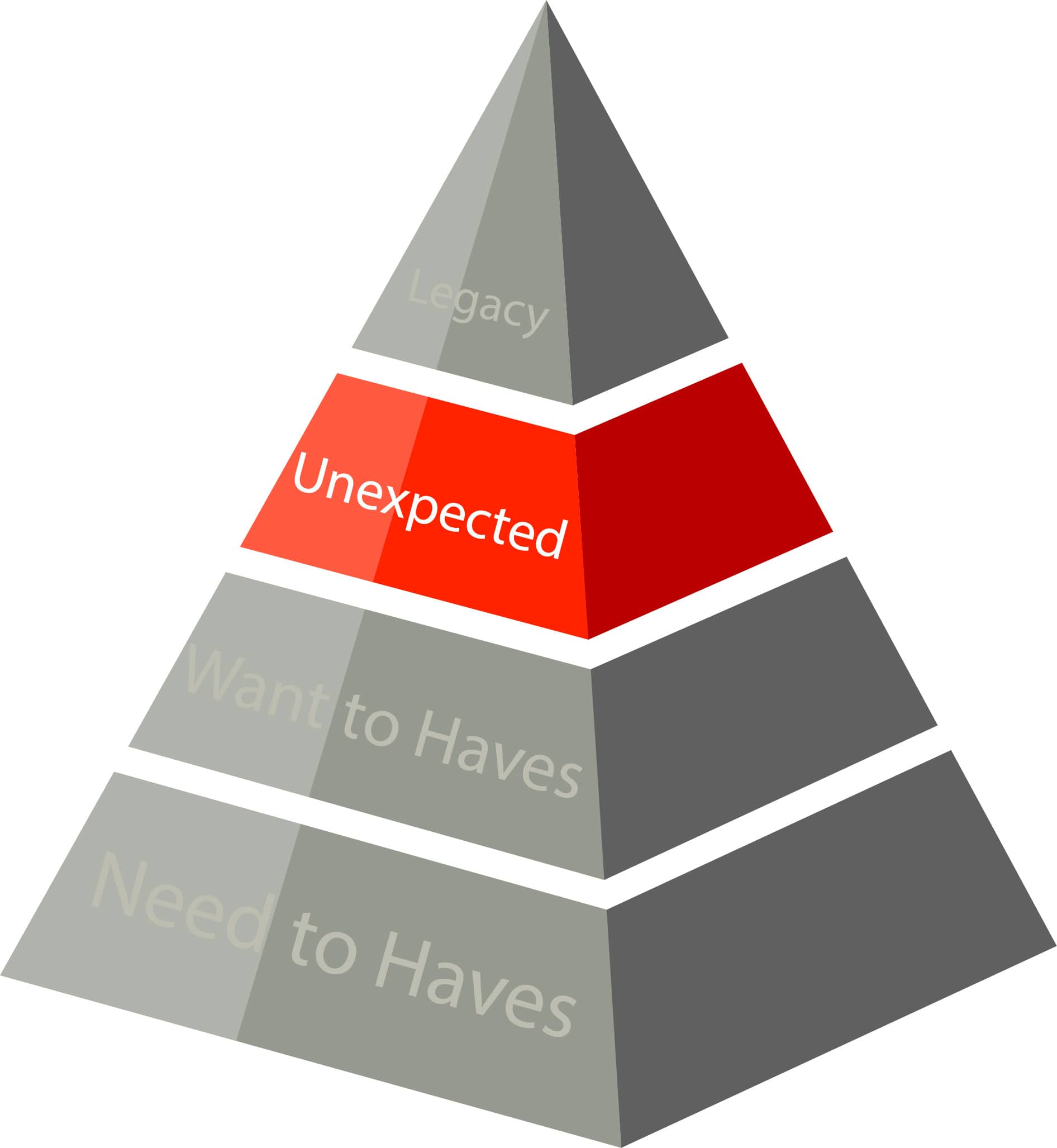

The Retirement Hierarchy of Needs, Part 3

This blog post is the third, in a series of 4, on what we at Tarkenton Financial call the “Retirement Hierarchy of Needs.” The Retirement Hierarchy of Needs is a philosophy of how to build a comprehensive financial plan for a client. The idea is to make sure to cover all of the needs, wants, and risks that may arise in a client’s retirement. Let’s look at the hierarchy.

With each tier of the hierarchy comes different types of expenses or goals for the money. You work with the client to determine how much money you need to allocate to each tier. In each post of the series, we will look at a different tier. We will discuss what expenses or risks are included in that tier and look at different ways to solve for those expenses.

If you read the previous posts, linked here and here, you are familiar with the different tiers. In today’s post we will cover the “Unexpected” tier. These are the, potentially catastrophic, expenses that we can’t see coming or, at least, can’t predict when they come. This can include long term care expenses, funeral expenses for a loved one or yourself, and, potentially, lawsuits. All of these are big enough that they could completely derail a sound retirement income plan, if they are not addressed. So, let’s address them.

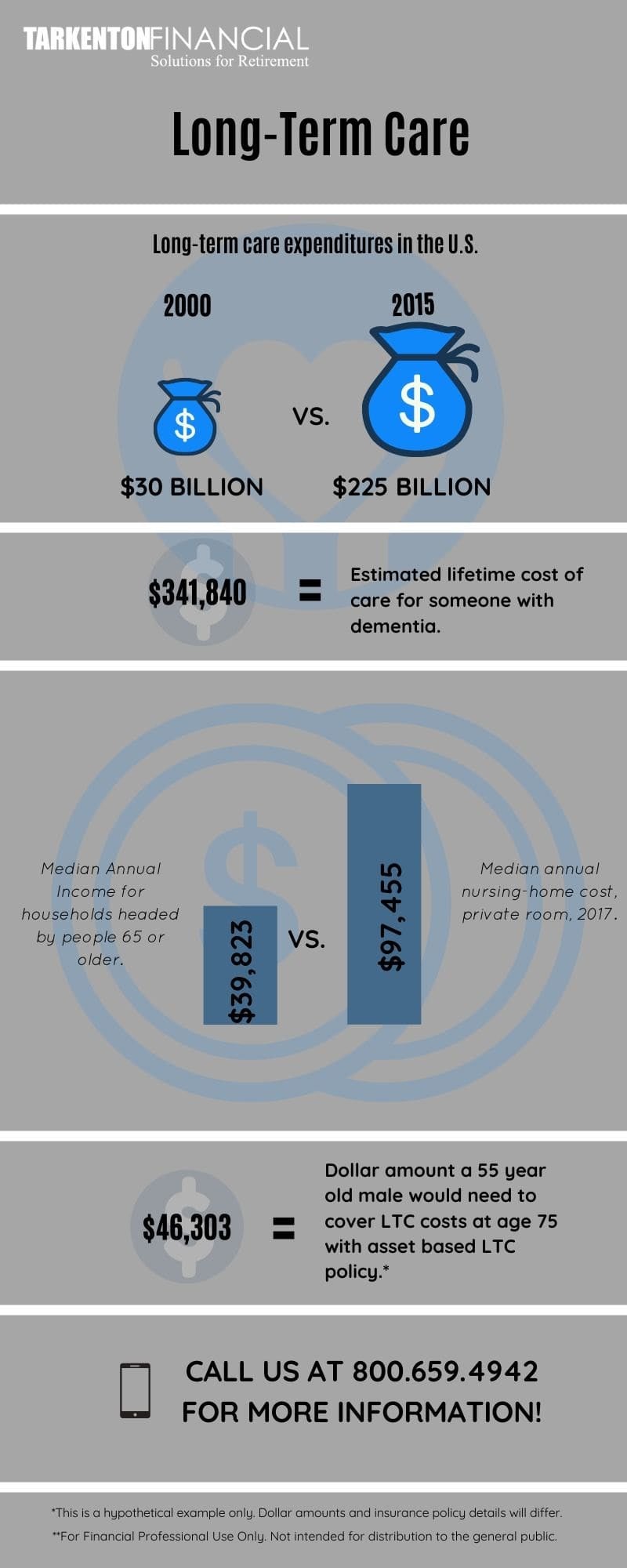

Rather than looking at a grid or chart of different numbers, like we have in previous posts, let’s focus on a few key LTC facts. The info-graphic below will lay them out for you but I would really like to point out that the average out-of-pocket cost for care, for someone with dementia is $341,840. And the gap between median annual income of a 65-year-old couple (or older) and that of the average priced private room at a LTC facility is $57,632 a year. If we can take $46,303 today and put it in an asset-based LTC policy (assuming 55-year-old in standard health) and solve for that gap, for 6 years, at age 75, wouldn’t that be worth it?

Thanks for reading,

Dustin Casebolt

Director of Advisor Development