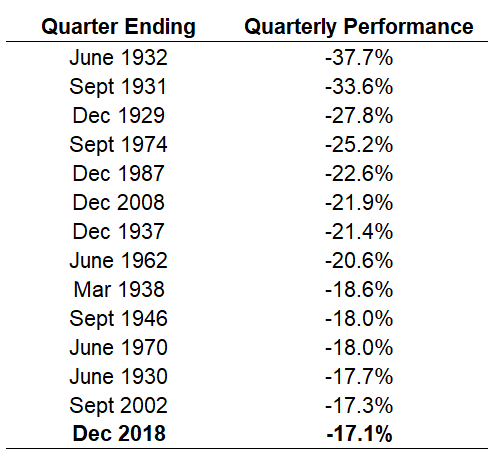

These past few months in the markets have been a roller-coaster ride, with volatility spiking and many investors feeling like they have experienced financial whiplash. With emotions running high for investors who have received some pretty discouraging December brokerage statements, we as financial advisors need to determine how we can effectively communicate to them the value of fixed indexed annuities in their financial world when they have just seen large declines in their account values. And make no mistake about it, the December of last year ranks historically near the top of the list when it comes to really bad months in the stock market:

The last time we had a month this bad in the markets it was December of 2008. I remember at the time thinking that many people who had paid little attention to fixed annuity solutions when the markets were going straight up would now be wanting to flee to the safety of the annuity. What I found, however, was that the trauma of the losses they had experienced tended in many cases to freeze them into inaction, much like a deer caught in the headlights of a car does not move even though they very much should. And so, the question is: how do we motivate people to action in a time of high market volatility. Here are a few thoughts.

Remind Them That Volatility Is Normal

When we talk with potential clients, it is important for them to realize that the end of year market selloff is not a temporary volatility pothole on the road to financial prosperity. The reality is that volatility is the norm in investing. It always has been and always will be. The remarkably low volatility in 2017 allowed many investors to think they had arrived at some kind of a “new normal.” The truth is that 2017 was more of the exception, and 2018 was more of the rule. Let me explain.

Standard deviation is one way to measure volatility. Since 1957, the long-term average standard deviation has been 15.6%. While 2017 had an amazingly low standard deviation of 6.7%, 2018 was only slightly higher than the historical average, coming in at 15.9%. In other words, if your potential clients are unnerved by volatility but think that the past few months have been an anomaly, you need to help them understand that the bumpy ride of recent months is far more the historic norm than not.

Fidelity Investments has published studies which found that, since 1920, the S&P 500 has on average experienced a 5% pullback three times a year, a 10% correction once a year, and a 20% bear market decline every three years. These 5% and 10% annual pullbacks have occurred even in years when the markets ended up to the positive. In spite of these regular corrections, markets have still generated positive returns over the long run.

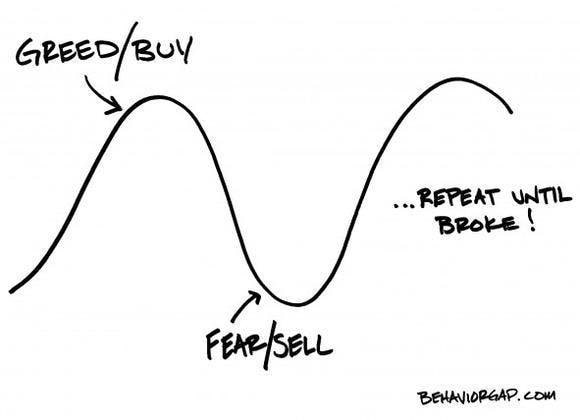

It has been my observation that for many clients who are risk averse, the high level of volatility that they have been exposed to by their advisors will not in the end serve them well. Given enough time the markets will generally head in a long term positive direction, but if the risk a client is exposed to creates short term losses that are more than they can bear, they are very likely bail out when the market bottoms out, stay in cash while the market recovers, buy back in when the market is peaking, and then repeat the cycle until they are broke.

I often say that the goal of retirement planning is about aligning a client’s dollars with their dreams, their portfolio with their passions. If they have a risk disconnect between the level of risk they are truly able to bear and the level of risk they are actually currently exposed to, we have an opportunity to help them.

Help Them Make the ROI Pivot

The materialistic culture that we are in can have tendency to make risk-averse clients feel that success is all about accumulating as much money as possible and that whoever dies with the most toys is the winner. Their portfolios as they approach retirement at age 55, 60, or 65 often resemble something an aggressive 30-year-old would have. Our job is to help them get past the day dreams of riches to focus on the real world of ever increasing longevity requiring ever lengthening streams of retirement income. Statements like the following might help:

- “When you were younger, ROI stood for return on investment. Now that you are older and approaching retirement, those same three letters should now stand for reliability of income. My life’s work is helping people like you do that very thing.”

- “At this stage of your life, you have far more to lose from a bear market than you have to gain from a bull market. In the work I do, we are not seeking potential as much as we are predictability.”

- “Because you are a responsible man, when you were younger you purchased life insurance in case you did not live long enough and your family would run out of money. Now that you are older, you need to purchase an annuity in case you live too long and you run out of money.”

It helps that the academic research is very much on our side. With the statistical risk of today’s retiree running out of money never having been higher, annuities are increasingly being seen by academicians as vital to a well-designed retirement plan. One very important study that you need to be acquainted with came from the American College in 2012. In this study, American College looked at the statistical likelihood of a 65-year-old retired couple running out of money if they were withdrawing 4% per year in inflation adjusted income. They looked at over 1000 different asset allocations, analyzing each with over 200 Monte Carlo simulations, and what they found was that a portfolio with a significant fixed annuity allocation had the highest likelihood of success for that 65-year-old couple. The bottom line is that annuities are not perfect financial products but they can be amazing tools in helping clients achieve the goal of not running out of money in retirement. Our job is to communicate clearly and persuasively to help them see that value.

Help Them Focus on Income for Life

The optional income riders that are available on most fixed and fixed indexed annuity products today are the chief supporting actors in the income story (the client is always the main actor!). How we position these products and demonstrate their worth to a client will, in many cases, determine as to whether the client takes action and integrates them into their retirement plan. Let’s look at the three key questions we need to be able to answer for clients when they are considering an income rider: What are they? What is their value to a retirement? Are they worth the cost of the fees that are charged?

What are they? Although they come in many shapes and sizes, income riders at their core are designed to give a client a contractual promise from an insurance company that a stipulated amount of income will be paid to them for the rest of their life, even if the account balance were to go all the way down to zero. There is typically both a deferral guarantee and a withdrawal guarantee built into an income rider. In the years that the annuity is being left alone to grow there is an income account value that is growing each year. (We need to be very clear with clients that this income account value is not available as a lump sum withdrawal in the way that their account value is). When they are ready to begin income, a withdrawal rate is applied to that income account value to determine how much income the client can enjoy.

What is their value in retirement? So much of what is done today in retirement planning is based upon projections: “If the market does this, and if inflation does that, then retirement will be a comfortable one for you.” Income riders on an annuity are based not upon projections, but upon predictability. Consider a hypothetical scenario. Let’s say you have a 55-year-old client who wants to retire in 10 years at age 65. He has $250,000 that he places in a fixed indexed annuity with an income rider that has a 6% annual rollup during deferral and a 5% withdrawal guarantee when he begins to receive income. In 10 years, the income account value would be $447,711. A 5% withdrawal guarantee would produce $22,385 in annual income that the client could not outlive, assuming he abides by the terms of the annuity contract. Ask yourself: is there any other financial product that can, with that degree of predictability, produce that much in guaranteed future income?

Are they worth the cost of the fees that are charged? You probably have heard clients ask the question, “Why do I need an income rider when all the insurance company is doing is sending me my own money?” Well, that is absolutely true, and the client would be correct in thinking that they could withdraw their own money for income from lots of other financial products without paying the fee associated with an annuity income rider. But in a world of exploding longevity and increasing economic turbulence, will those other products continue to send them a check each month even if there is a zero balance in the account? That is the value of the income rider. I tell my clients that I am a believer in worst case scenario planning. We can hope for the best, but it is important to plan for the worst. When you hit a zero balance in any other financial product, the worst case scenario is that there is no money left in the account and the income that is needed for retirement stops. With a fixed annuity with an income rider guarantee, only the first part of that worst case scenario would apply, because the income checks would continue for the rest of the client’s life.

Let me offer an analogy. Imagine you were going to go sky diving. You drive to a sky diving school and, after signing lots of documents that state that if you end up doing an imitation of a pancake on the airport tarmac you blame no one but yourself, you reach for your checkbook to pay the $200 fee. As you are about to fill in the dollar amount, you nervously look up and ask the flight instructor, “Has anyone ever died doing this?” He answers you by saying, “Yes. A few people have died, but there is a 98% chance that your chute will open and you’ll be fine…however, for an additional $20, you can rent an extra backup chute that would give you a 100% chance of your chute opening.” Let me ask you: after hearing that, would you be writing a check for $200, or for $220? I thought so. Me, too. That is the value of an income rider. Without it, the client may very well never run out of money. With it, they can rest assured knowing that they won’t.

Conclusion

While volatility may be a normal thing in the markets, it need not be a reason for our clients and potential clients to miss out on the increased stability and reliable income that can come from the quality annuity offerings that we as financial advisors can offer to our clients. Please contact your marketer at Tarkenton Financial to learn about the products that will help your clients rest assured that they will have income throughout retirement, and download the sales piece on Taking Pressure off Your Portfolio.

Sincerely,

Shawn Moran